What's the point of holding Bonds?

Credit Suisse has published an article (which we have reproduced in full) explaining why it’s appropriate to continue holding bonds in a low or negative yield environment.

Approximately 30% of all bonds traded globally, have negative yields. Buy a bond with a negative yield, hold it to maturity, and you will lose money. It is one of the few things you can be guaranteed of in the financial markets. With interest rates steadily marching downwards and central banks around the world locked in a race to see who can keep their rates lowest, surely then the outlook for bonds as an asset class is bleak at best. We disagree with this negative take on bonds. Switzerland, for instance has had negative rates for some time, yet year to date its bond market has returned over 12%. Not only that, its bonds continue to act positively in equity sell offs, stabilising portfolio values.

It is important to understand what is driving global rates and bond yields lower across the globe. Since the GFC, central banks have been buying bonds in the name of quantitative easing (QE), to push yields down. Yield is the cost of borrowing for the issuer. With borrowing costs down, central banks have been hoping to generate economic growth.

What was meant to be an emergency measure has taken root. Low to negative yields are and continue to be a long-term reality. QE, flat wages growth and ageing populations have each contributed to this. What the Swiss, Japanese, and the European Central Bank have done in pushing yields down in their regions, is to force bond investors to look elsewhere. Low yields have been exported to other countries. International bond investors look at the yields on offer in the US and Australia and are buying. Investors have also been buying riskier bonds in the search for yield.

The dual role of bonds in a multi asset class portfolio is income and capital stability. For Australian bond investors, low yields do not change that. Although the often quoted 10 year Australian Government bonds are trading at a low yield to maturity of around 1%, they should form only part of the bond allocation. A portfolio including state government and corporate bonds will enhance the yield on offer. Investment grade bonds issued by non-cyclical companies have attractive qualities. Issues from government supported agencies also provide some yield gain. Investors can also consider credit from low risk issuers that is further down the capital structure and so attracts a higher yield. For example, the big 4 banks are currently issuing tier 2 subordinated debt at a significantly better yield to their own senior debt. What each of these bond types have in common is they should do well in an economic slowdown. It is wrong, to buy riskier, bond like investments to earn a higher yield, and assume they will provide capital stability in a risk sell off.

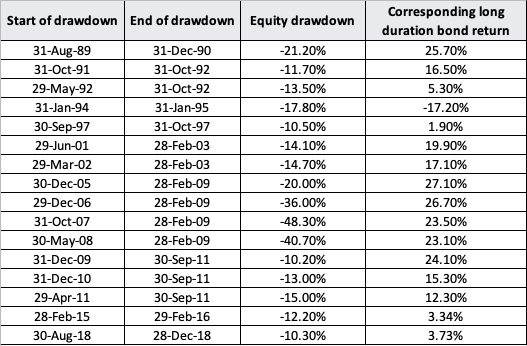

A concern often voiced is falling yields have seen bonds and equities rise at the same time, and so bonds won’t provide the same protection against an equity sell off as they have in the past. It is true that both bonds and equities have risen in 2019, however, this is not unusual. In fact, looking at the return of Australian shares and long duration Australian bonds, each calendar year since 1999, there have been 14 out of 21 occasions when returns have been in the same direction, both positive and negative. The true worth of bonds as a portfolio stabiliser occurs when there is a sharp sell off in shares. In the table below we note each draw down top to bottom of more than 10% since 1989 in Australian shares, and the corresponding return of the AUD 10+ yr Government Bond Index.

Australian Equity Drawdown and 10 Year Government Bond Returns

Source: Credit Suisse, Bloomberg - ASX All Ordinaries Accumulation Index and 10+ yr Government Bond Index

In 15 of the 16-share market sell offs, bonds have provided a positive return, including just last year. We expect this relationship to continue. Correlations between bonds and equities move around depending on market conditions. Below we graphed the rolling one-year correlation between 10 year AUD Government bonds and Australian equities. The correlation remains negative.

Australian Equity-Bond Correlations – Remain Negative

Source: Credit Suisse, Bloomberg - All Ordinaries Accumulation Index and Australian 10 Year Government Bond Total Return Index

An issue we may have to deal with in the future is zero cash rates in Australia accompanied by our own quantitative easing, that pushes the 10 year government bond yield to zero or into negative territory. We would be surprised if this was necessary but the RBA have openly been discussing this scenario in order to achieve their unemployment and inflation targets. In such a situation, would we be as confident of the stabilising qualities of investment grade bonds? We have no precedent for this in Australia but we can look to the experience of Switzerland to inform our view. Switzerland has been dealing with negative official cash rates since 2011, and negative yields on their 10 year government bonds since January 2015. We asked our Swiss colleagues if Swiss bonds had lost their stabilising attributes in share market sell offs? The short answer was no. The following table shows Swiss share market drawdowns of 10%, or close to, since cash rates went negative, against the return on Swiss 10 year Government bonds over the same period.

Source: Credit Suisse, Bloomberg – SMI Price Index and Swiss 10+ yr Government Bond Index

It shows that in spite of close to zero or negative yields, Swiss 10-year Government bonds still performed well relative to the return on equities in times of share market stress.

Australian bonds are delivering on their dual objectives of income and portfolio stability. But investors have to accept the income from bonds will be lower than the past. Although 10-year yields on Australian bonds are low, there are still opportunities to achieve a better income return with a diversified bond portfolio. In addition, the evidence both here and overseas shows bonds continue to provide capital stability with yields low or even negative, as is the case in Switzerland.

Author: Andrew MMcAuley: https://www.livewiremarkets.com/wires/what-s-the-point-of-holding-bonds