Shares vs Sydney houses - which wins?

Property as a lifestyle asset vs investment asset

In recent decades, Australian residential property has shifted from being solely thought of as a lifestyle asset – a place to live with family – to increasingly being a financial asset. Houses have always been a way to display wealth, but when did they become a path to generate it? Government policy has supported this structural shift[i].

For many Australian investors, especially those who manage their own investments, buying property is often the default choice. Through conversations over time, several common reasons emerge:

Real estate is tangible and easier to understand.

The perceived returns are comparable to those from investing in shares.

It is seen as a low-risk investment.

There are tax deductions that can be claimed.

As rates of home ownership fall, renters struggle to make ends meet and central banks run out of policy space, will property continue to be an attractive investment option for Australians? And has property been a strong performer relative to alternatives like share portfolios in recent times?

In this article, we aim to constructively challenge some assumptions and paint a more realistic view of reality.

How do property prices perform over the very long-term?

The very long-term performance of residential property tends to track closely with inflation. This is because one of the primary drivers of property prices is household incomes, which are closely tied to inflationary trends.

For instance, Norway, a country with similarities to Australia in terms of limited available land and high wealth, saw real house prices (adjusted for inflation) decline from 1900 to 1950, only recovering their inflation-adjusted 1900 levels just before 2000[ii]. Similarly, a graph tracking US house prices throughout the 20th century illustrates that prices generally lagged inflation from 1890 to the 1940s. Post-World War II, housing demand surged (due in part to the baby boom), temporarily boosting prices before stabilising to match inflation rates for the remainder of the century. However, just before the Global Financial Crisis (GFC), prices spiked sharply, influenced partly by legislative changes under the Clinton administration that encouraged increased bank lending for housing, only to later correct[iii]:

Is residential property a substitute for shares?

When it comes to investing surplus income, individuals typically face two primary options: buying an investment property or starting a share portfolio. While both have their merits, a closer look reveals that shares offer several advantages over property.

Between July 1991 and May 2023—a span of 30 years—the median Sydney house price grew from $221,770 to $1,253,759. In absolute terms this looks spectacular, but in percentage terms it equates to an average annual growth rate of 5.76%[iv].

Over the same period, the Australian stock market delivered an average annual return of 9.15%. The U.S stockmarket’s average annual return was 10.07%[v].

The difference between the end value of a portfolio growing at 9.15% per annum and one at 5.76% per annum over 30 years is a significant +157% in favour of the share portfolio.

Of course, not all Sydney residential properties grew at the same rate. Not all houses in the same street experience the same capital growth. And the returns above ignore net rental income.

But as capital values increase, rental yields fall over time. Many sources estimate the average Sydney rental yields around 3.0% at present. When you subtract strata costs, insurance, interest costs, council rates, and potentially land tax, the net rental income can become immaterial. An investor becomes largely reliant on capital growth for their investment return.

Beyond investment returns, the advantages of a share portfolio can also outweigh the benefits of investing in residential property, as discussed below:

Advantages of Investment Property vs Shares

Tangible and Familiar - Investing in bricks and mortar often feels more comfortable, especially if you lack expert advice on building a share portfolio that aligns with your objectives.

Geared returns? – because banks are willing to accept property as security for debt, investors can magnify their returns (both up and down). You can also borrow to invest in shares, but banks will lend more, and at lower interest rates, against residential property. However, you will need a bigger deposit to get started with a loan for property compared to shares.

Tax deductions – Purchasing a new property may provide depreciation benefits, but it's important to note that interest on borrowings for both property and shares is tax-deductible.

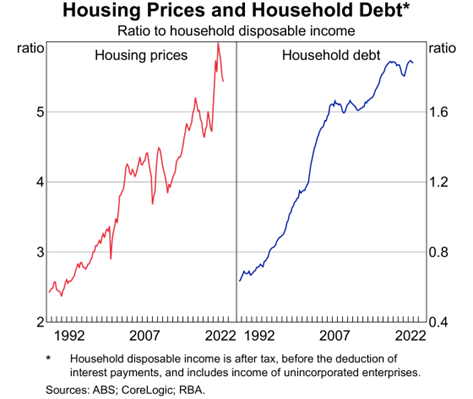

Perceived Stability - Property price volatility is less transparent than in the share market, making fluctuations less noticeable. However, as the RBA graph below shows, house prices are indeed volatile and can mimic stock market movements, although the stockmarket has greater potential for short-term declines.

Advantages of a Share Portfolio vs Residential Investment Property

Lower Upfront Costs - Trading costs for shares are approximately 0.15%, compared to 5.0% or more for purchasing an investment property (including stamp duty).

Lower Exit Costs - Selling shares incurs around 0.15% in costs, versus 2.0% or more for property (including agent fees and marketing costs).

Liquidity - Shares can be liquidated in 3 business days, while property sales will take at least 6 weeks to settle, plus the marketing campaign period.

Low Initial Capital - Starting a share investment requires minimal upfront dollars.

Avoid rectification work – there has been a growing list of apartment buildings subject to major rectification work, even in upmarket suburbs. Being involved with your strata committee to resolve this not only consumes time but can impact the property’s price. Consider this unit block in Neutral Bay - https://mosmancollective.com/general/uncontrolled-cracking-discovered-in-luxury-neutral-bay-apartment-block/#:~:text=The%20state's%20building%20watchdog%20has%20uncovered%20serious%20defects%20in%20a,complex%20at%209%20Young%20St.

Lower ongoing costs - Unlike property, where ongoing costs like repairs and maintenance are inevitable and unpredictable, a share portfolio doesn’t require additional capital unless you choose to participate in corporate actions like Share Purchase Plans. If investing in shares via a managed fund or ETF, ongoing costs can be relatively low and are known up front.

Partial Redemption - You can sell part of your share portfolio, unlike property, where you can’t sell just one room at a time.

Consistent Income - A diversified share portfolio can provide regular income, whereas rental income may fluctuate, especially during tenant vacancies.

No Tenant Issues - Avoids the stress and potential mental strain of dealing with problematic tenants.

Minimal Time Commitment - Managing a share portfolio typically requires far less time than handling property-related tasks like agent coordination, rent collection, and maintenance.

Franking credits – are a tangible benefit of investing in a diversified portfolio including Australian companies. Every year franking credits can be used to offset tax liability and, in some situations, effect a refund of excess franking credits.

Diversification - A share portfolio allows for diversification across multiple assets and geographies, whereas buying property ties your investment to a single asset.

Price Transparency - Share prices are updated daily, providing greater certainty.

No Land Tax - Unlike property investors, share investors are not burdened by land tax, which is an increasing concern in the property market. Note land tax is not deductible against your income.

Land Tax is a growing issue

In Australia, the Valuer General in each state determines the "unimproved" value of land annually. While your primary residence is exempt from land tax, this tax applies to other properties, excluding land used for primary production. In NSW, the land tax structure is:

No tax on the first $1,075,000 of land value, then $100 plus 1.6% of the value above $1,075,000.

For land holdings exceeding $6,571,000, a flat rate of $88,036 is applied, plus 2% of the value above $6,571,000.

Historically, these thresholds were indexed annually, but the NSW Government has announced from 2024, these thresholds will be frozen, leading to an increase in the number of people paying land tax over time.

In Victoria, the situation is more concerning due to recent changes. Victorians who own a second home or investment property now face a $500 annual tax for properties with a land value between $50,000 and $100,000. This tax increases to $975 for properties valued between $100,000 and $300,000, plus an additional 0.1% of the land value for properties worth more than $300,000.

Traditionally, there has been a significant gap between the Valuer General's estimates and the market value of land. However, this gap is narrowing. For instance, land values recorded by the NSW Valuer General increased by 26.3% from 2021 to 2022. We have a client whose land valuation surged by 50% in the past two years alone.

In our analysis for some clients, we've found that land tax on investment properties can consume most of the net rental income, leaving the investment's return heavily reliant on capital gains.

Housing affordability at current levels

Investors looking at investment properties need to consider what future returns may look like. Assuming returns over the past 30 years will be replicated over the next 30 years may be misleading.

Many factors have led to an undeniable housing crisis in Australia.

The Demographia International Housing Affordability report for 2023 shows Sydney is the second least affordable major global city, only behind Hong Kong. People living in Sydney need 13.3 times the median income to afford the median house price. Australian markets overall have a median multiple of 8.2, up from 6.9 in 2019.

Rising debt levels have been a contributing factor to rising house prices. The RBA provides data illustrating the strong correlation between rising housing prices and increasing household debt over the past 30 years:

However, while household debt has surged, wage growth has not kept pace with escalating house prices[vi]:

As a result, housing has become less affordable, leading to the growing reliance on the "Bank of Mum and Dad." The average borrower now needs 46% of their income to service their mortgage—a near-record high. Just three years ago, this figure was 29%, thanks to historically low interest rates. At current prices, many people simply cannot borrow enough to buy property:

Since the early 2000s, the difference between the median dwelling price, and what the average Australian can borrow, has grown. As of July 2021, the real median dwelling value was $656,694, but the average borrowing capacity was about $400,000 – a difference of more than $250,000. How long does it take the average Australian to save $250,000?

One recent study found that a Sydneysider earning the median income of $1,500 per week could not afford to buy a unit anywhere in Greater Sydney. Even in the cheapest suburbs of western Sydney, unit prices were just above the affordability threshold used in the analysis, and houses were far beyond reach.[vii].

Reforms that previously appeared politically infeasible – such as higher property taxes, limits on mortgage credit expansion, or some form of public housing program – may gain traction.

All of this leads to a fundamental question: if people are already struggling to purchase property at current prices, what will drive property price growth over the next 30 years?

What conclusions can we draw?

For investors with substantial assets, a mix of shares and investment property can be a prudent strategy. However, for many, residential property might be better viewed as a lifestyle asset. Opting for a low-cost, diversified share portfolio to build wealth can be advantageous for several reasons:

Lower Costs - Shares have lower upfront, exit and ongoing costs.

Liquidity & Flexibility – you can redeem any amount within 3 business days.

Diversification – you can quickly build a low-cost share portfolio holding 10,000+ global securities. With property, you own one house in one street.

Expected returns – historically it can be reasonably shown the stockmarket has outperformed Sydney residential property. Current borrowing capacity restraints and potential reforms to improve housing affordability could be headwinds for future price growth.

Time commitment – time is one thing you cannot buy more of, and managing a residential property investment will inevitably absorb more time vs a share portfolio.

Author: Rick Walker

Please share this article with anyone you think would benefit from reading it.

[i] When home earn more than jobs: the rentierization of the Australian housing market by Josh Ryan-Collins & Cameron Murray, November 2021

[ii] Source: ‘Long-run house prices,’ The Australian, 23 May 2010

[iii] Source: GMO

[iv] CoreLogic Property Pulse from August 2022 estimated house values increased 5.8% pa over average over the 30 years since July 1992, which is consistent with this figure.

[v] As measured by the S&P 500 Index.

[vi] Sydney property prices: Why the odds are stacked against first-home buyers (afr.com)

[vii] Two experts measured how bad Sydney’s property market is. They got a shock (smh.com.au)