The Numbers Don't Lie - Most Fund Managers Fall Short

Every six months, Standard & Poor’s (S&P) releases its SPIVA (S&P Indices Versus Active) Scorecard — a long-running report that compares how active fund managers stack up against their benchmarks. The latest edition, covering 20 years of data to the end of 2024, reinforces a message we’ve shared for years: most active managers (the stock pickers and market timers) underperform. Consistently.

This isn’t just a financial industry view. Nobel Prize-winning academics like Fama, Markowitz, Sharpe, and Miller have long argued that market timing rarely produces reliable returns. SPIVA’s latest data backs that up — showing that short bursts of outperformance tend to fade, and underperformance becomes more pronounced the longer the time frame.

The Numbers: Australia and Beyond

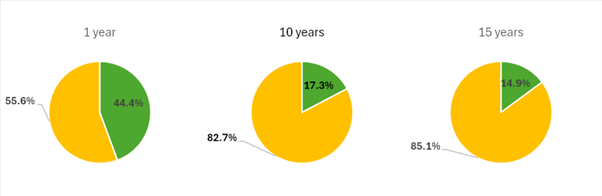

Australian equity managers had a relatively good run in 2024, with 44% outperforming the ASX 200. But stretch the lens to 10 and 15 years, and only 17% and 15% respectively have beaten the index. The longer the horizon, the harder it is to stay ahead:

Source; SPIVA report. The green pie are the outperformers

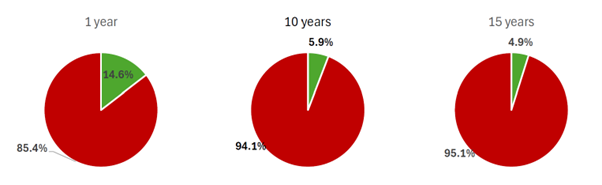

Managers of international equity funds fared worse. In 2024, 85% underperformed the S&P World Index. Over 10 years, that figure climbs to 94%, and over 15 years to 95%. That's a long time to be wrong.

Morningstar reports that the average active manager investing in international shares charges 1.14% p.a. Meanwhile, a diversified global portfolio can cost as little as 0.35%. It begs the question — why pay extra for a lower chance of success?

There’s a well-documented link between fees and returns: the higher the fees, the lower the returns. And yet, high-fee active managers continue to pitch outperformance as their value proposition.

SPIVA Cuts Through the Spin

What makes the SPIVA Scorecard so useful is that it doesn’t just compare raw returns. It adjusts for two major distortions that can make active managers look better than they are:

Survivorship Bias: Over the past 15 years, 57% of Australian-managed funds (domestic and international) were shut down or merged — often removing poor results from the public record.

Style Drift: If a manager strays from their mandate (say, a growth fund buys small-cap value stocks), SPIVA reclassifies the fund to reflect its actual strategy. That way, the comparison is apples to apples. For example, when adjusted for style drift and risk, the 44% of Australian equity managers who outperformed in 2024 drops to just 30%.

What It All Means

The bottom line: market timing and stock picking, even by seasoned professionals, struggle to outperform over time. And once you apply proper statistical analysis, most of the so-called “skill” looks a lot more like luck.

At Lorica Partners, we base our investment approach on evidence, not predictions. The core of our client portfolios are constructed using globally diversified, low-cost funds — and we assess performance using data that cuts through the noise, so we can focus on what really drives long-term returns.

Author: Rick Walker

Source: S&P Global, "SPIVA Australian Scorecard Year-End 2024